PCPS Succession Institute 2016 Succession Survey Results Part 1 – Solo Practitioners & Sole Proprietors

This article summarizes selected results of the Private Companies Practice Session (PCPS) and Succession Institute (SI) 2016 Succession Planning Survey (the full survey results available through the PCPS Resource Center). This is the fourth such survey conducted since 2004. Of the Solo Practitioners (68 having only one person in the firm) and Sole Proprietors (316 having more than one person in the firm) responding, the following tables and commentary summarize the results and our conclusions, from practice continuation agreements through sale or merger of their practices.

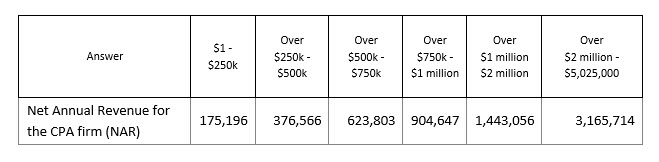

Below is a table of solo and sole proprietors that provided Net Annual Revenue data. We broke out the responses in a way to create groups of meaningful data. The last category stops at $5.025 million because that was the largest firm that was classified as a Sole Proprietor.

Survey respondents represented a great deal of diversity within each group.

This year’s survey generated some interesting comparisons with past survey results. It also provided some additional information to enhance one’s understanding of the status of succession planning at this time within the CPA profession.

Historically, few sole proprietors have had practice continuation plans in place, and once again, it does not appear that they have made any headway in this regard.

I currently have an existing practice continuation agreement with another firm:

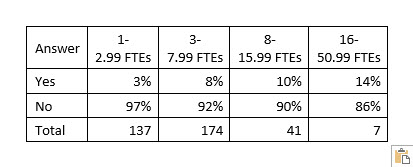

Regardless of firm size, not very many firms have practice continuation agreements in place. However, as firm size grows, the existence of practice continuation agreements increases as well. Clearly there is a big jump in agreements at 3 FTEs and above.

Regardless of firm size, not very many firms have practice continuation agreements in place. However, as firm size grows, the existence of practice continuation agreements increases as well. Clearly there is a big jump in agreements at 3 FTEs and above.

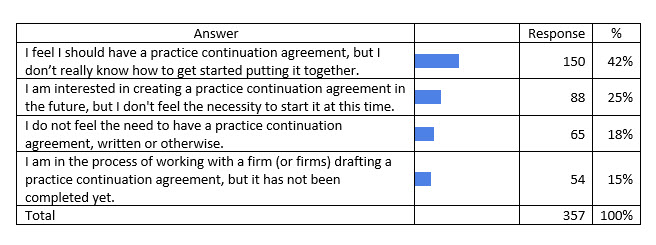

For those that DO NOT have an existing written practice continuation agreement with another firm, which most closely reflects the status:

For those that DO NOT have an existing written practice continuation agreement with another firm, which most closely reflects the status:

Of the 93% of firms that do not have a practice continuation agreement, 57% feel the need for one but don’t know how to get started or are in process of drafting one. And only 18% of this group don’t feel a practice agreement is necessary. So from our perspective, there is strong awareness of the need for agreements, but clearly making this happen is still too low of a priority for the vast majority of solo practitioner and sole proprietor firms.

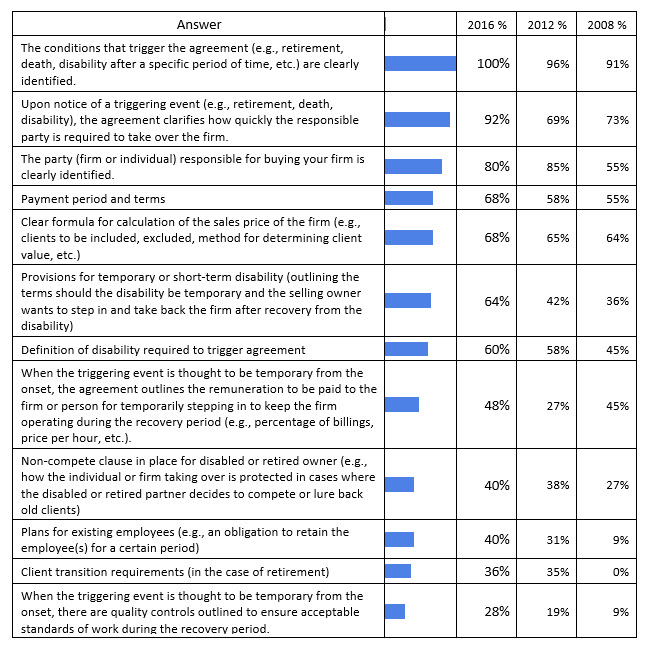

For those firms that do have practice continuation agreements in place, we asked what topics are covered in their practice agreements. The following table shows the topics covered in existing practice continuation agreements, compared with prior years’ responses. With the exception of one of the responses, all of them are trending in a positive direction from previous years, with many making significant improvements in this year’s survey.

The three provisions that took big jumps this year were:

- Upon notice of a triggering event (e.g., retirement, death, disability), the agreement clarifies how quickly the responsible party is required to take over the firm.

- Provisions for temporary or short-term disability (outlining the terms should the disability be temporary and the selling owner wants to step in and take back the firm after recovery from the disability).

- When the triggering event is thought to be temporary from the onset, the agreement outlines the remuneration to be paid to the firm or person for temporarily stepping in to keep the firm operating during the recovery period (e.g., percentage of billings, price per hour, etc.).

Each of these jumped at least 20%, with the differences between 2012 and 2016 being 23%, 22% and 21%, respectively.

This year we asked several new questions about succession plans or exit strategies, which our tables will show below. We will start this section off with the question that asks the broadest succession question, which is, “What best describes your current plan?” We changed this from our previous surveys to reflect the options we currently are seeing in the marketplace (we added a common option we see, which is to merge your firm in your last four to five years prior to exiting and plan on working for the combined firm for a number of years in full-time and then possibly part-time roles). We also eliminated the choice of selecting all of the options because we felt this response allowed people to sit on the fence rather than share the path they are most likely going to take.

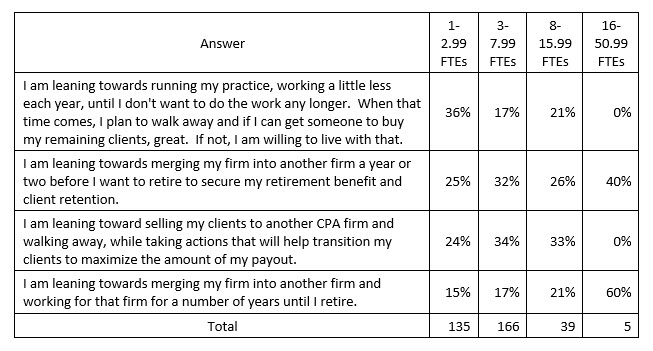

The following best describes my succession plan, retirement plan, or exit strategy (shown by FTE):

100% of firms with 16 people or more are only considering a merger option, while firms with 3 people or less are the most likely to adopt the “turn the lights off as I leave” strategy. What seemed strange at first was the number of firms with more than 3 and less the 16 FTEs that were the most likely to exit quickly when they decide to go and either sell their clients to another firm and walk away (highest percentage) or merge-in long enough just to transition their clients. But then on further reflection, these choices are lining up logically. For the smallest of firms, when the owners decide they want to leave, they just want to be done. As the firms grow larger, the owner’s asset (firm value) becomes more significant and more complex (sustaining revenues, taking care of long-time clients, providing a new home for staff, the assets – like equipment, furniture, a lease or ownership in a building, etc.) and the longer the owner is planning on staying involved with the new firm to help with the transition as well as protect the value of that asset.

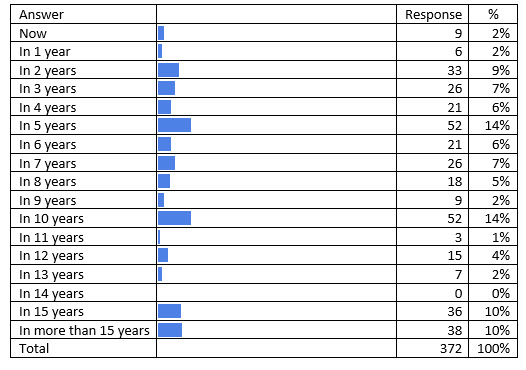

Next, with some new questions, we wanted to better understand when people planned to retire, using two questions. The first was about the number of years until an owner plans to retire (to understand the amount of transitions likely to occur in the near future) and the second question was to find out the age at which the owner plans to retire. There was some interesting information in these answers.

What is your approximate planned timing to fully retire or exit your practice?

The average number of years until retirement for the group was about 8 years. That breaks down to about 20% in the next 3 years (from now to 3 years), another 20% in the following two years (years 4 and 5), and another 17% in years 6 to 8 years. A total 40% of the Solo Practitioners and Sole Proprietors plan on retiring in the next 5 years. Based on some recent AICPA firm statistics, considering that our profession has roughly 44,000 firms, with only 585 having 21 professionals or more, we can conclude, based on these survey findings, that:

- The merger market for small firms is about to heat up substantially with lots of opportunities for small firms to grow larger via merger very quickly if they are prepared

- The marketplace is likely to get very soft towards the end of that 5-year period because 1) there is a limit as to how many firms a mergor firm can bring in at a time without overloading its capability to manage the growth and transition, and 2) we can expect, consistent with the supply/demand consequences taught in Economics 101, that when supply exceeds demand, price drops.

This takes us to the next question about planned age of retirement.

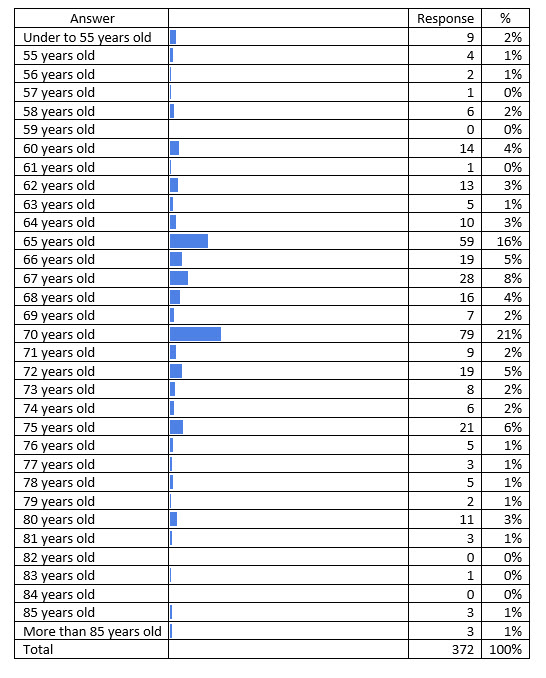

At what age are you expecting to fully retire or exit from the practice?

This table shows a definite message that our Solo Practitioners and Sole Proprietors are planning on retiring at ages older than the owner mandatory retirement ages we find in multi-owner firms. The average retirement age for this group is 68, with 48% of the respondents planning on retiring at age 70 or older, 17% planning on retiring younger than 65, 29% planning on retiring between age 65 and 67, and another 6% retiring at ages 68 and 69. When you consider the number of solo owners that plan on using the “turn out the lights” strategy, it makes sense that people plan to work longer, cutting back their hours as they get older, and working until they just don’t want to do it anymore.

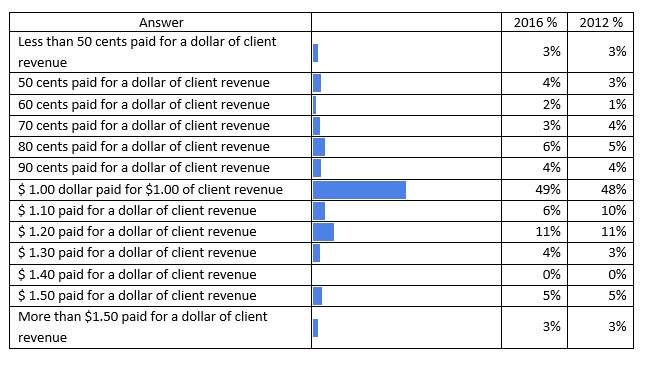

Solo Practitioners and Sole Proprietors were asked what they expect to receive in return for their client book or firm at retirement. Twenty-two percent of the respondents expect less than $1 for $1 (up two percent from 2012) of billings, and nearly half, 49% (48% in 2012), expect $1 for $1 of billings. 21% expect between $1.10 - $1.30 for their clients (down from 24%). All in all, the results are virtually the same as in previous surveys inasmuch as all of these variances are not significant and could easily be explained away as selection bias (because people self-select as to whether to fill out the survey rather than samples being statistically drawn to represent each of the groups we want to analyze).

The dollar amount I expect, as a ratio of client billings for my practice, is:

For firms with 16 FTEs or more, 71% have an expectation of paying/receiving a $1 for each $1 billed and collected from/for their clients. Compare that 71% to the average of 48% expecting the same amount for firms with less than 8 FTEs. For firms with less than 8 employees, 65% believe a range of 80 cents to $1.10 is the market rate for client books, whereas 78% of the firms with 8 to less than 16 FTEs feel that same range is market rate. This compares with 100% of firms with 16 FTEs or over that believe this range represents market rate.

When asked about the time period they expected to receive their payouts, 66% of the respondents indicated a period of three to five years. Another 6% are looking at one to two years, with 13% expecting to be paid in full at the time of sale. There is an “N/A” in the column for 2012 because we didn’t provide this as a possible response. Although many solo owners are expecting to be paid up-front, survey results show that the buyers are following a different playbook than the sellers are anticipating.

The number of years over which I expect to be paid for my practice:

Only 14% of the respondents felt like a payoff period of more than 5 years was likely in both 2016 and 2012. The biggest change between the two surveys is that there is a 5% drop between 2012 (43%) and 2016 (38%) as to the percentage of respondents who believe that 5 years is the likely payoff period. But given that 13% expect to be paid in full at time of sale in 2016, that difference had to be allocated to the other options in 2012. Surprisingly only 3% additional expected a 1-year payoff in 2012 (we would have expected all of it to show up there), 4% in a 2-year payoff, and 5% in a 5-year payoff.

Firms with 16 or more FTEs expect to either be bought out on the date of sale (hopeful, but rare) or in 5 years or 10 years. With firms in the 8-less than 16 FTE range, half think that 5 years is the most likely payoff period, with another 8% in 3 years, 8% in 7 years and 18% in ten years. But with firms with less than 3 FTEs, 51% expect to be paid in full by the end of 3 years, and 91% by the end of 5 years. This all makes sense because payment terms in the marketplace are all over the board. The smaller the firm and the smaller the overall amount owed, the more quickly acquiring firms would just want to pay it off and get it behind them, especially when the owners that are selling their firms are no longer involved in the practice (either working or transitioning clients) after the first two years. In converse, the larger the selling firm, the bigger the financial obligation to the selling owner, and the more likely the payment terms will be stretched out.

To summarize, as is the case with expectations for receiving more than $1 for every dollar of revenue billed, we believe that it is unrealistic to expect to receive a buyout over a payout period of less than four to five years unless the size of the client book being purchased is very small. As well, solo owners can expect their payout to be contingent on client retention by the acquiring firm, together with a possible ceiling where the amount paid will not exceed whatever the selling CPA generated in fees or total book leading up to the time of sale, regardless of what the buyer can generate in fees with that same book of clients. Finally, based on our experience, and certainly any deals we have been involved in, our clients (the buyers) don’t sign personal guarantees for any purchases and seldom put money down upfront. These are normally “pay as you go” transactions with the payments to the seller only being made after fees have been billed and collected.

The next three new questions were asked to understand the difference between expectations and market conditions. We first asked solo owners what their expectation was for financing the sale of their firm (or client book). That was followed by a question of the same group asking who in that group had actually acquired a firm (which was 62 out of 366 respondents). Next we asked only the 62 respondents how they had actually financed the acquired firms. There were no surprises to us in the responses. However, many of our solo owners will definitely be surprised.

Which best describes your expectation regarding financing the sale of your firm?

16% of solo owners are expecting to be paid in a lump sum upfront for their firms or client books. Another 46% (38% plus 8%) expect the purchase price to be set at the time of sale without consideration of retained clients, with 38% of that group expecting a down payment. But at least this group expects to be paid out over a number of years instead of a lump sum. 35% (28% plus 7%), down payment or not, expect to be paid based on client retention over a number of years.

Now, let’s take a look at this group and see who has actually participated in an acquisition.

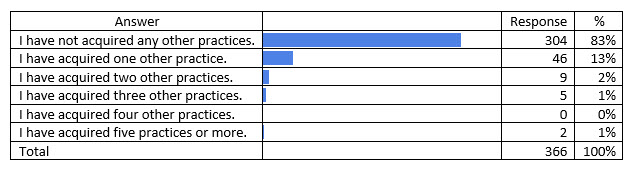

Which best describes the number of practices you have acquired in the past four (4) years?

62 respondents (17%) have acquired from 1 to more than 5 practices in the last four years, with 46 (74%) of those having acquired one practice during this period. So, we asked this group … “How did you buy those practices?”

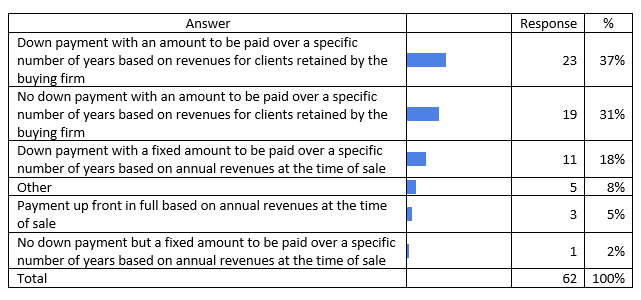

Which best describes your approach to purchasing the firms you have acquired?

37% of those who had acquired firms paid a down payment and then made payments based on clients retained over a specific number of years. 31% made payments based on client retention, but did not make a down payment. Either way, down payment or not, the solo owner is only receiving an amount based on retained clients. Together, 68% of those acquiring firms based the acquisition payout on client retention. 20% (18% plus 2%) paid a specific price set at date of sale paid over a number of years (with the 18% making a down payment while 2% did not). Only 5% paid for the clients upfront. The 8% of responses falling into the “Other” category were mostly a mixture of some formula related to client retention or selling the firm internally over time to new owners.

The point in all of this is that 16% of solo owners are expecting a lump sum payment at the time of sale although only 5% of buyers actually are doing that. 46% of solo owners are expecting a selling price set at time of sale paid out over time, while only 20% of buyers made that offer. And 35% of solo owners expect to be paid based on client retention while 68% of the acquisitions occurred in that manner.

If there was a surprise to us it would be that 25% of the buyers were willing to pay based on a price set at the time of sale. Only one of our clients to our knowledge has done this and the circumstances were that they were purchasing a very small firm (about $300,000 in revenues), they discounted the revenues by 50%, and wrote a check for $150,000. So, while this meets the “pay a lump sum based on revenues at the time of sale” criteria, our belief is that the seller in this case would have been better off being paid out over time based on collections. However, it was a unique situation and the seller’s circumstances didn’t allow that.

The bottom line is that there is a wide-gap between what solo owners expect to receive for their practices as well as the terms of the deal compared to what the market is currently doing. And as noted above, as more firms sell when the baby boomers start to retire en masse, the survey shows current practices, not what likely will be available five years into the future.

We will pick up here next time as we get into some of the findings for the multi-owner firms which will take several columns to cover. But as you can see after reviewing highlights of the survey results regarding solo practitioners and sole proprietors, you can expect our profession to undergo some dramatic changes over the next 5 years and that story will continue to hold up as we review the data for multi-owner firms as well.

Download

| File |

|---|

| PCPS Succession Institute 2016 Succession Survey Results Part 1 - Solo Practitioners & Sole Proprietors |

We help organizations implement their unique strategies by:

• Working with them through the tough issues, and

• Customizing responses to address root causes, rather than merely treating symptoms.