PCPS Succession Institute 2016 Succession Survey Results for Multi-Owner Firms Part 5

This article summarizes selected results of the Private Companies Practice Session (PCPS) and Succession Institute (SI) 2016 Succession Planning Survey (the full survey results available through the PCPS Resource Center). This is the fourth such survey conducted since 2004. Part 1 of this column series covered the results for Solo Practitioners and Sole Proprietors. Part 2 covered Demographics, Succession Plan Status, Ownership Retirement projections, and Firm Infrastructure. Part 3 started with Mandatory Retirement and concluded with the calculation of the original valuation of the retirement benefit. Part 4 reviewed how firms might adjust the original valuation benefit based on actions or inactions of the retiring partner. We pick up this column, Part 5, by discussing policies for transitioning client relationships and continuing through the challenges firms are trying to address that represent barriers to your firm's effective succession management.

Policies for Transitioning Client Relationships

In this year’s survey, we provided an expanded set of options for firms to pick from with regard to client transitioning policies. As a result, we learned that 44% of the 387 firms responding to this question have not addressed transitioning of client relationships.

As with past surveys, when owners are two or three years away from retirement, about 30% (2016—30%, 2012—32%, and 2008—32%) of the participating firms require them to start transferring clients under a plan set out by the firm.

Similar to prior years, about 20% (2016—21%, 2012—18%, 2016—17%) of the firms require the retiring partner to transition client relationships to people chosen by the firm’s managing partner. New this year is the statistic on required transitioning of referral sources, of which 27% of the firms require.

Due to the expanded set of answer options and relatively low number of responses to many of the options, no other significant trends emerged in this year’s survey.

It is interesting that 74% of multi-owner firms expect succession planning challenges within the next five years (see section Status of Succession Planning), yet only 44% have addressed client transitioning at this time. Putting it off will only make matters worse. In our experience, we find that discussing policies like this when no one is close to retirement generates the most rational conversations. The closer to being “out the door” that someone is, the more the discussion regarding policies like this may be perceived as the firm trying to claw back some benefits the retiring partner is ready put in the bank.

We suggest that firms not delay in addressing this and related issues. Whatever conflict your owner group experiences now will become exponentially greater with each year that you get closer to someone departing. Avoiding these discussions does not make them go away, but rather, as time passes, they will move from what would have been rational discussions to emotional confrontations augmented with personal hurt feelings and attacks.

When owners are two or three years out from retirement, which of the following describes your firm's practices?

As might be expected, if you look at all of the responses above by firm size, the larger the firm, the more likely it is that the firm will require transitioning of clients (part of the reason why the firms have grown to the size they are). Similarly, as firm size grows, generally the more we see the firm/managing partner selecting to whom clients are transferred, as well as providing financial rewards and/or penalties based on transitioning (see those survey responses shaded in gray). For example, once firms reach the 100+ FTE size range (47% and 31% respectively, at least more than double the responses of firms at any other size) the partners are removed from the standard compensation system and are rewarded financially for transitioning client relationships. We find that, if you don’t carve out special compensation plans for retiring owners to motivate them during the transition period immediately prior to retirement, you can expect those owners to continue to develop their relationships with their clients as they try to maintain their client service responsibilities and billings. This often results in poorly transitioned clients, and most damaging, retired partners who still maintain key client relationships in the firm.

As has been similar in the past, overall 21% (18% in 2012 and 17% in 2008) of the firms allow the retiring partners to choose to whom they transfer their clients. We always suggest that firms should ask the retiring partner for his or her suggestions as to who might be best suited to take over specific client relationships and be the most seamless fit, in the end, the firm is responsible for determining how their resources (partners) need to be utilized. To allow a retiring owner to have control over this critical of a process is to basically allow that person to determine how the remaining organization is going to operate in the future.

The counter argument comes from the retiring owner saying something like, “Since I will be penalized if the client is lost, I want to turn my client over to the person I think has the best chance of maintaining a long-term relationship.” If this is the case you have a problem on this side as well. The retiring owner needs to be held to a specific transition plan. If he/she follows the identified plan for each client, then whether the client leaves the firm or not there should be no penalty to the retiring owner. If the client leaves after proper transitioning, it is because the firm lost the client. On the other hand, if the retiring partner does not execute on the transition plan per the instructions articulated for each client, then the retiring partner should be held responsible (because he/she did not give the firm an adequate chance to keep the client) for any of these improperly transitioned clients that subsequently leave. This balanced approach is equitable: the retiring owner is protected if he/she does the right things, and the firm is protected if it does the right things.

Succession Strategies

Which describes the transition of your firm when the current senior owner(s) retire?

Some new answer options were added to this year’s survey as well as some of the previous options revised slightly. Consequently, comparability with prior years has been affected.

This question changed from prior years because we shifted it from “select all that apply” to “choose the best answer.” In the past, it was fairly apparent that while the vast majority of firms planned to sell internally, they also had a “wait and see” approach as options for sale and merger were also of high interest if the senior partners did not perceive that the younger partners are stepping up and living up to their expectations. We changed the question because we wanted to know more definitely what the plan was. Certainly, regardless of the primary option, if things don’t work out, all options are on the table. But we were not sure whether merger/sale was the primary option with the back-up being selling internally, or vice versa. Seventy-six percent of the 392 firms plan to sell the firm internally to the remaining owners, with 11% having no idea (a new option this year), and 10% more planning on merger. This is a strong showing for remaining independent given the merger mania existing in the marketplace over the past decade.

As a side note, we believe that if the senior partners are not seeing their younger partners stepping up and living up to expectations, there’s a high probability that it is because the senior partners have made one or more of the following mistakes. They:

- made people partners who shouldn’t have been admitted as partners in the first place, or

- haven’t spent the necessary time developing their younger partners, or

- have not been making the necessary investments into building infrastructure and capacity to sustain the firm beyond the senior partners, or

- haven’t gotten out of the way long enough to find out what the younger partners have to offer.

As we always say, whether it is in our books or videos or speaking in public settings, while the senior partners can and should take a great deal of the credit for the exceptional successes their firms have enjoyed, they can equally take the blame for the firm’s shortcoming because they are either not addressing or are poorly addressing the areas in question.

The above table essentially shows a continuation of past findings: the larger the firm, the higher the expectation that ownership will be transitioned internally (from 56% at a low for the smallest firms and a 97% average for the largest firms [an average of 51 FTEs or more at 97% + 94% + 100% divided by 3]). Smaller firms, while apparently desiring to see the transition occur internally as expected, are still contemplating merger (at 17% for firms with less than 8 FTEs). And the smaller the firm, the more likely that the partners have NOT addressed this issue yet (21% and 15% for FTEs of less than 8 and less than 16 respectively).

Have you been in active merger or acquisition discussions with a firm (or firms) in the past 24 months, or are you planning on looking into merger or acquisitions in the next 24 months?

Up somewhat from past years (44% in 2012), 51% of the 396 firms answering this question have been actively discussing mergers or acquisitions/sales in the past 24 months or are considering looking into them over the next 24 months.

Up somewhat from past years (44% in 2012), 51% of the 396 firms answering this question have been actively discussing mergers or acquisitions/sales in the past 24 months or are considering looking into them over the next 24 months.

Which best describes your role in the merger and acquisition discussions you have been having?

This question was answered by 191 of the 193 firms that are actively looking into mergers. Consistent with the previous year’s survey results (62% in 2016 and 64% in 2012), nearly two-thirds are doing so as an acquirer with roughly one out of five (18% in 2016 and 21% in 2012) looking at both sides of the merger transaction—both as an acquirer and as a potential target for acquisition. Therefore, 80% (62% + 18%) of the respondents are looking to acquire other firms.

Now, let’s take a look at these two questions by size of firm to see how the numbers skew by size.

Have you been in active merger or acquisition discussions with a firm (or firms) in the past 24 months, or are you planning on looking into merger or acquisitions in the next 24 months?

The larger the firm, the more likely it has been considering a merger or sale/acquisition, with 73% or more of firms who have 51 FTEs or more indicating that they have been in active discussions or are planning to engage in such discussions. If you assume (just based on our experience) that 51 FTEs would correlate on a low end to about $5 million in revenue (51 FTEs times $100,000 per FTE at a low end), that means that 3 out of 4 firms over $5 million in revenues have (in the last 24 months) or will (plan to have in the coming 24 months) active discussions about merger/acquisition regarding their firms.

The larger the firm, the more likely it has been considering a merger or sale/acquisition, with 73% or more of firms who have 51 FTEs or more indicating that they have been in active discussions or are planning to engage in such discussions. If you assume (just based on our experience) that 51 FTEs would correlate on a low end to about $5 million in revenue (51 FTEs times $100,000 per FTE at a low end), that means that 3 out of 4 firms over $5 million in revenues have (in the last 24 months) or will (plan to have in the coming 24 months) active discussions about merger/acquisition regarding their firms.

Which best describes your role in the merger and acquisition discussions you have been having?

We wanted to take a look at this from an FTEs and revenues perspective. As you can see, firms above 101 FTEs or $25 million in revenues are only considering being the mergor. Firms from 51 FTEs to less than 101 and those from $8 million to less than $25 million are still looking at both options. And everyone smaller than $8 million, except for firms less than $500,000 in revenues, are looking at both options.

What is the targeted size (in annual revenues) of firms you are looking to acquire?

This is a new “select all that apply” question added to the survey this year. For firms of all categories, merger targets of 10% to 30% of the acquiring firm’s annual revenues are fairly common. In the smallest size category, the greatest apparent interest lies in mergers with firms equal to about half of the acquirer’s revenue. As we expected, there are very few firms looking at trying to acquire and merge firms larger than theirs.

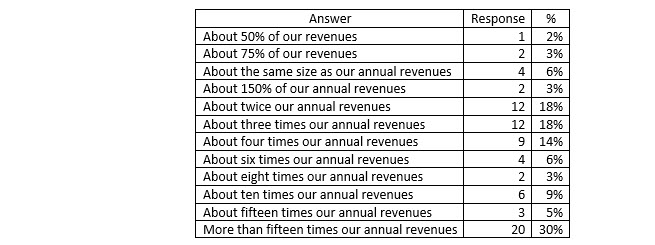

What is the optimum size of the acquisition targeted (in annual revenues) for firms you are looking to acquire?

What is the optimum size of the acquisition targeted (in annual revenues) for firms you are looking to acquire?

Once we had asked about acquiring firms as a percentage to their size, we then asked what were the annual revenues of the firms they were looking to acquire. So between the first question and this one, we gain an insight as to size proportional to the acquiring firm as well as revenues of interest to those firms. Firms with volumes between $300,000 and $1.5 million have the most interest overall in the merger/acquisition marketplace with the average for this question falling between $750,001 and $1,500,000.

Once we had asked about acquiring firms as a percentage to their size, we then asked what were the annual revenues of the firms they were looking to acquire. So between the first question and this one, we gain an insight as to size proportional to the acquiring firm as well as revenues of interest to those firms. Firms with volumes between $300,000 and $1.5 million have the most interest overall in the merger/acquisition marketplace with the average for this question falling between $750,001 and $1,500,000.

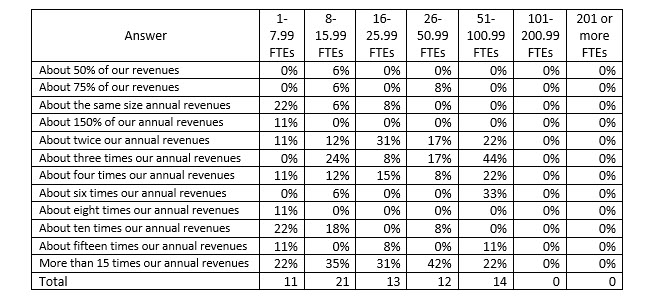

But a different story is told when you look at this next table which breaks this question down by firm size.

Now you can see that firms under 16 FTEs are most interested in merging or acquiring firms at $750,000 or less, with firms with 16 FTEs and less than 26 FTEs are most interested in firms from $300,000 to $1.5 million. Firms from 26 FTEs to less than 101 are most interested in merger/acquisitions from $750,000 to $3.5 million. Firms with 101 FTEs to less than 201 FTEs are most interested in firms from $1.5 million to $15 million, and the largest of firms are most interested in merging in firms from $3.5 million to $25 million. So while the overall average firm of interest for merger or acquisition is in the size range of $750,000 to $1.5 million, this is due to the greater volume of firms in our profession being smaller firms. But as you can see, as firms grow larger, the optimum merger/acquisition target grows right along with them.

Now you can see that firms under 16 FTEs are most interested in merging or acquiring firms at $750,000 or less, with firms with 16 FTEs and less than 26 FTEs are most interested in firms from $300,000 to $1.5 million. Firms from 26 FTEs to less than 101 are most interested in merger/acquisitions from $750,000 to $3.5 million. Firms with 101 FTEs to less than 201 FTEs are most interested in firms from $1.5 million to $15 million, and the largest of firms are most interested in merging in firms from $3.5 million to $25 million. So while the overall average firm of interest for merger or acquisition is in the size range of $750,000 to $1.5 million, this is due to the greater volume of firms in our profession being smaller firms. But as you can see, as firms grow larger, the optimum merger/acquisition target grows right along with them.

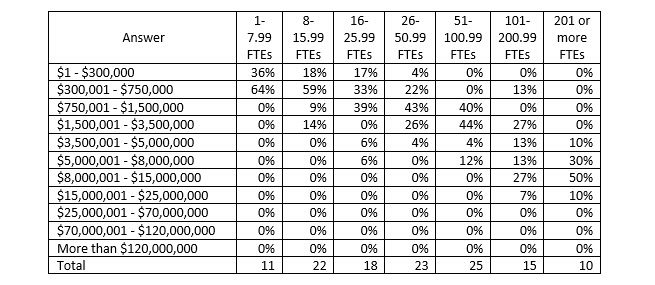

What is the size (in annual revenues) of firms that have been looking at acquiring you?

Of the 66 firms which responded that they were in merger discussions as the mergee, the proportional size of the mergor firm (the firm interested in acquiring or merging their firm) to their firm was as follows.

Of the 66 firms which responded that they were in merger discussions as the mergee, the proportional size of the mergor firm (the firm interested in acquiring or merging their firm) to their firm was as follows.

As noted earlier, firms with 101 FTEs or more were not engaging in these discussions as the mergee, and that is reflected above. But we were surprised that firms of almost every size were interested in merging/acquiring firms with less than 8 FTEs. The data also shows that 22% of these firms (with less than 8 FTEs) indicated firms more than 15x their size were in merger discussions with them. It is interesting to note further that a fairly large level of interest (ranging from 22% to 42%) is being shown by firms 15 times the size of the firms in every size category (except for firms with 101 FTEs or more). Firms about twice the size of the acquisition targets account for a range from 11% to 31% of responses.

As noted earlier, firms with 101 FTEs or more were not engaging in these discussions as the mergee, and that is reflected above. But we were surprised that firms of almost every size were interested in merging/acquiring firms with less than 8 FTEs. The data also shows that 22% of these firms (with less than 8 FTEs) indicated firms more than 15x their size were in merger discussions with them. It is interesting to note further that a fairly large level of interest (ranging from 22% to 42%) is being shown by firms 15 times the size of the firms in every size category (except for firms with 101 FTEs or more). Firms about twice the size of the acquisition targets account for a range from 11% to 31% of responses.

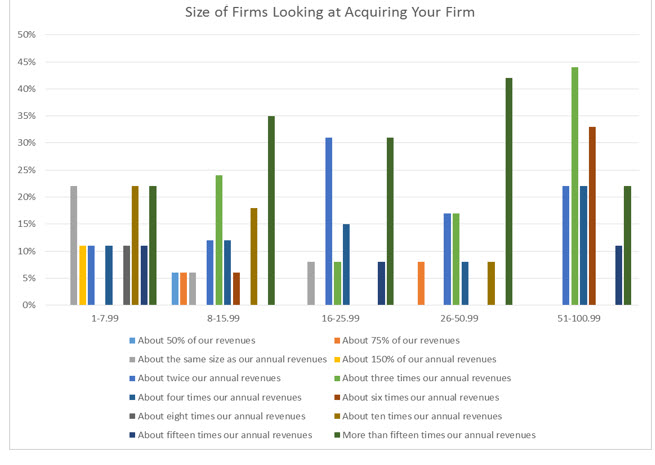

We developed the following graphic by firm size to more clearly display the relative size of firms who have been approaching them for merger or acquisition.

What challenges you are trying to address that represent barriers to your firm's effective succession management?

What challenges you are trying to address that represent barriers to your firm's effective succession management?

The options for answers to this question were expanded this year, so overall comparability has been affected because of that. However, from the 384 responses answering this question, two issues clearly can be viewed in terms of trends: lack of penalties for improperly transitioning clients (23%), and concern about the next generation’s readiness to take over (33%). But the real trend here is that firms are getting better at managing succession issues, with or without a plan, as overall the numbers in each question are either about the same or trending in a more positive direction.

The options for answers to this question were expanded this year, so overall comparability has been affected because of that. However, from the 384 responses answering this question, two issues clearly can be viewed in terms of trends: lack of penalties for improperly transitioning clients (23%), and concern about the next generation’s readiness to take over (33%). But the real trend here is that firms are getting better at managing succession issues, with or without a plan, as overall the numbers in each question are either about the same or trending in a more positive direction.

In reviewing the table showing data by firm size, one will note that the three middle size ranges covering 16 to less than 26 (34%), 26 to less than 51 (32%) and 51 to less than 101 FTEs (33%) are struggling the most with not having a penalty for improperly transitioning clients.

With respect to whether the senior partners feel that the younger members are ready to step into their shoes, the table shows surprisingly that firms from the size of 26 to less than 201 FTEs (45%, 53%, 47% respectively) are having the most difficult time with this. Generally speaking, our experience is that the larger the firm, the less this is a problem. But even for firms from 101 to less than 201 FTEs, almost 50% of the firms said this was a problem.

Although these opinions about the lack of readiness among the next generation of partners could be valid, we often find diamonds in the rough in such situations that just need some polishing to prepare them for leadership. In these and other cases, it not uncommon that the reason senior owners don’t have people on board with whom they’re comfortable is because the senior partners have not taken the time to develop the people below them. Or just as common, the current leaders don’t see the emerging leaders stepping up because the current leaders won’t get out of the way.

The fact is that firms only need, and only can handle, so many leaders at any one time. Therefore, until a leadership void is created or becomes available to be filled (we recommend that existing leaders create those openings), it is highly likely that no one will step up. Often the future leaders won’t step up out of respect for the existing leaders. It is not because the future leaders are unwilling to do the work necessary; these young leaders don’t want to appear to be pushing the existing leaders aside. The good news, however, is that if a firm has at least a three-year window to conduct the necessary deferred maintenance in leadership development, much can be done to remove this perceived barrier to success.

And the biggest surprise of all is that firms with 101 to less than 201 FTEs, 41% are having trouble getting retirement age partners to retire (and therefore 41% probably are having trouble getting them to transition clients). When the highest percentage of acknowledgement of this issue for the other sizes of firms is 15%, 41% is clearly a significant proportion.

The fact that firms in all size ranges, except for the largest size category of FTEs, have no mandatory retirement age points to future problems for them in succession management. The good news is that this statistic is trending in the right direction. The problem we encounter regularly is that when the senior owners are doing their job to create strong future leaders, but the senior owners decide to stay around on an indefinite timetable, the firm will often lose some of their most promising succession candidates. These people will leave either to start their own firms or to go to work in another firm in order to find a home with more certainty as to exactly when they will be able to step into the senior leadership roles.

A piece of good news in this year’s findings is that 23% of the firms indicate that their succession plan is in place and working well, where the larger the firm, the more likely this response was selected (with 31%, 47% and 38% respectively for firm with 51 FTEs or larger). However, even with this positive progression, there are still a lot of firms who need to do anywhere from a little to a lot of work in succession management.

We were also happy to see the downward trend of retired partners still being allowed to manage a significant number of client relationships. From our experience, however, we still find this situation in almost every size firm we work with, except for the largest firms that don’t allow retired partners to work in the firm at all after retirement. Regardless of firm size, rarely does any good come from having retired partners maintain client relationships after they are sold their ownership. It most often will lead to the firm being held hostage by these retirees with the retirees ending up double-dipping by earning extra compensation post-retirement to do what they should have already done pre-retirement.

Wrap-Up

We will pick up at this point in the survey for our next column, Part 6, as the survey addresses the People Side of Succession. This column will provide insight into requirements for new partners, changing infrastructure and developing future leaders.

Download

| File |

|---|

| PCPS Succession Institute 2016 Succession Survey Results for Multi-Owner Firms - Part 5 |

We help organizations implement their unique strategies by:

• Working with them through the tough issues, and

• Customizing responses to address root causes, rather than merely treating symptoms.