PCPS Succession Institute 2016 Succession Survey Results for Multi-Owner Firms Part 3

This article summarizes selected results of the Private Companies Practice Session (PCPS) and Succession Institute (SI) 2016 Succession Planning Survey (the full survey results available through the PCPS Resource Center). This is the fourth such survey conducted since 2004. Part 1 of this column series covered the results for Solo Practitioners and Sole Proprietors. Part 2 covered Demographics, Succession Plan Status, Ownership Retirement projections, and Firm Infrastructure. We pick up this column, Part 3, sharing tables and commentary summarizing the results and our conclusions starting with Mandatory Retirement and continuing through the original valuation of the retirement benefit.

Mandatory Retirement or Sale of Interest

Of the 410 firms responding to this question, only 35% said that their agreements set a mandatory retirement age. Responses to this question have varied in the past surveys, from 41% in 2004, to 48% in 2008, to 47% in 2012, and at 35% in 2016 (although it shows up as 32% in the “select all that apply” question above regarding partner agreements, with that difference likely being explained in the following two ways. The first explanation would be that were more responses to the question showing a higher percentage – 410 as compared to 397 -- and 2) because some people might have more casually reviewed and skipped over options from the long list of partner agreement policies/procedures versus when it was asked specifically asked by itself). Based on results of four surveys covering a dozen years, it would appear that some firms are doing away with the mandatory requirement for partners to sell their ownership at an age-specific date.

Which is true regarding your firm? Mandatory Age:

What is the mandatory age for partners to sell his or her ownership interest?

For the firms that said they do have a mandatory retirement age, we asked them to share what their age for mandatory sale is. The average, based on all of the responses to this question is 67 years old. 45% said that 65 years of age is the mandatory date for a sale or retirement, with 9% selecting age 66, and 9% more selecting age 67. With 7% selecting social security age, this represents a total of 70% (45% + 9% + 9% + 7%) having a mandatory retirement age range of 65-67 in 2016 versus that same range being at 72% (55% + 7% + 6% +4%) in 2012. In 2016, we see a slight increase with ages 68-70 totaling 21% (4% + 0% + 17%) as compared to 16% (2% + 0% + 14%) in 2012. All-in-all, the mandatory age for sale of ownership has remained virtually the same over the last 4 years, with the possible argument that some firms are letting the final age dates slide a year or two. However, it is very clear as the firm grows larger, the more likely the firm has included mandatory sale of ownership in their partner agreement (from 7% to 100%).

Policies and Accountability for Retired Partners

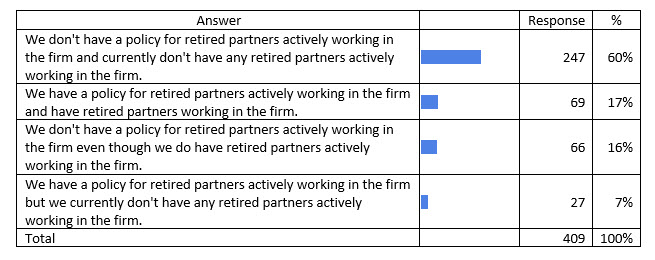

Do you have a policy outlining expectations, privileges, and accountability for retired partners actively working in the firm?

Sixty-seven percent (60% + 7%) of multi-owner firms don’t have any retired partners working in the firm after retirement. This seems high to us because most of our client firms have at least one or two retired partners still doing some work after retirement. However, many firms are still in their first generation of owners and no one has retired yet, so that could explain why this percentage is higher than we’d expect. In larger firms of $30 million and more, it is common to not allow partners to stay on after retirement. But in firms smaller than this, it is very common, and at least one or two of the founding partners are usually the first in line to leverage this privilege.

A total of 76% (60% + 16%) of responding firms don’t have a policy as to the possible roles, pay, and accountability for retired partners. In our experience all partners are reasonable when the discussion about rights and privileges is not about them, but rather, about others sitting at the table who might elect such an option. Therefore, the best time to put policies in place clarifying acceptable roles and pay for retired partners is when no one is on the verge of retirement. At the point that someone is in their last few years before retirement, this discussion seems to be more personal for the retired partner who may view it as if the policy is being created to limit and/or punish them. This situation makes the discussion as to best practices in this area far more difficult to have and typically results in a much less functional solution.

The most serious issue we see in the above table is when a firm has retired partners working in the firm and no policy (16%), which means there is no agreement as to how those relationships and expectations will be handled, when specific privileges will end, etc. We have worked with firms that had retired partners on the payroll who showed up to work and received a paycheck year after year even though the remaining partners had to redo their work and constantly intervene because the retired partner created problems by not following procedures, or by making inappropriate demands of staff treating staff in ways that were considered unacceptable, and more. When the partner group does not establish in advance the rules outlining the privileges and limitations for retired partners continuing to work, it is not uncommon for those firms to allow retired owners to get away with behaving badly for many years because the remaining partners want to avoid the conflict they know will occur when they finally ask the retired partner to leave. Because this experience is so common, the largest firms have already learned this and therefore tend to create policies that do not allow retired partners to stay (see section Mandatory Retirement or Sale of Interest). Our opinion is that many retired partners can provide great value to the firm after a sale of ownership, within clearly defined parameters. This is why we propose making this a win-win situation by allowing those who can still contribute, a privilege granted at the sole discretion of the remaining partners, to do so under one year agreements that do not automatically renew.

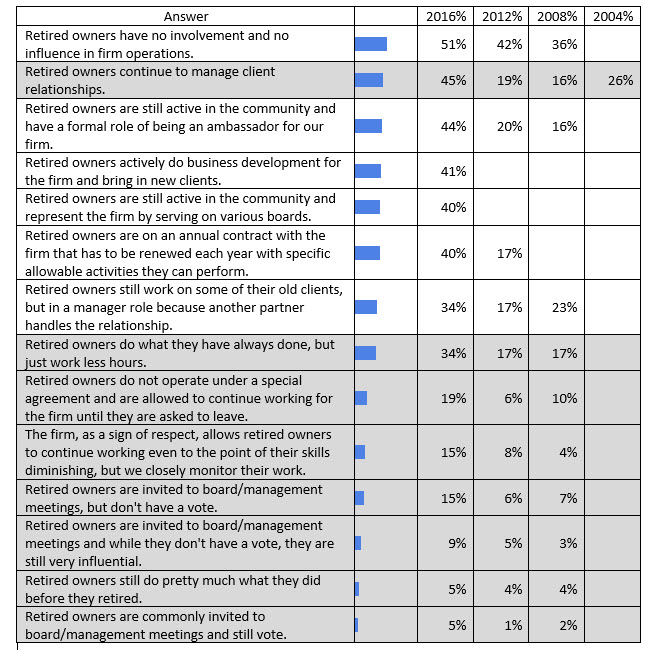

Which of the following best describes the involvement of retired owners in the firm? (gray shaded rows explained below)

There were 151 responses to this “select all that apply” question. If you don’t see a response for a question in a previous year, it is either because 1) we didn’t include that same statement in that previous survey, or 2) we phrased the statement differently enough that we felt it would be inappropriate to include it for comparison. However, if the statement was slightly different but in our interpretation it had the same meaning, we did include the previous survey results for comparison in the table above.

We see many good trends in the responses to this question. This is an example of firms making progress on their succession planning; even though many don’t have a succession plan, they are addressing critical succession issues. But what is interesting is that all of the statistics are trending up, both good and bad. Rather than list all those that are good and then do the same with those that are bad, we have highlighted in gray those practices that we believe should be stopped. For example, retired partners should be removed from the management of the firm so that the younger leadership can take over (and if the old guard leadership is still in attendance of those meetings, they can’t help themselves but to try and influence, and sometimes bully, the younger owners into doing what the firm has always done), so they shouldn’t attend board meetings and they certainly shouldn’t have a vote. As well, as we have stated before, retired owners should be directed as to what activities they should focus on post-retirement as well as removed from many duties, so allowing retired owners to do similar work to active owners will eventually undermine any firm’s succession efforts.

Setting up policies that clearly articulate what retired owners can and can’t do, and the exact roles they can fill post retirement is a critical area for firms to address now. Workload compression is not going to go away anytime soon. Therefore, most firms will want to keep quality talent (many retired partners would fit this description) at least on a part-time basis assuming the pay arrangement is fair for both sides (fair for the remaining partners as well as the retired partners). But retired partners should only be allowed to stay under the right circumstances with the right expectations, oversight and accountability.

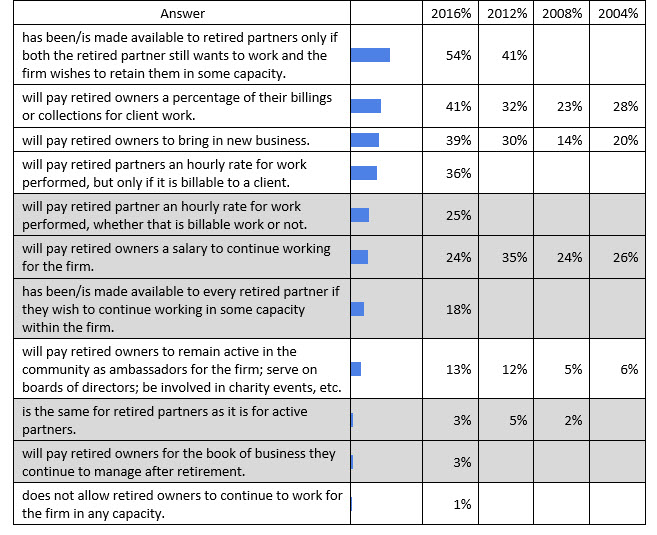

Which describes your current compensation plan for retired owners or owners that have sold their interest in the firm? Our firm's compensation plan:

With 158 responses, this question is similar to the last one because most of the trends were up, both the bad and good. We have highlighted in gray those practices that we believe should be stopped.

The first response that did not trend up was “paying the retired owner a salary,” which went down (from 35% to 24%), which is a good trend. The second response that did not trend up was “paying retired partners in the same way as active partners,” which went from 5% to 3% which is likely less of a trend and more likely due to selection bias. Fortunately, the response percentage to the second question is low for all of the years.

Finally, while the practice of “paying a partner by the hour for both billable and non-billable work” is shaded, it is only shaded due to the strictest interpretation of the response. There is nothing wrong with paying retired partners an hourly rate to serve in non-billable roles filling strategic issues such as training, sitting on boards, or doing special projects for the firm. Actually, we recommend doing this as part of the annual contract – specifically identify non-billable projects, create a budget for those functions, and pay an hourly rate. However, we often see the negative version of this practice most often where firms simply pay an hourly rate for all of the time that the retired partner sits in his or her office without regard to what they are doing or whether what they are doing is even of value to the firm.

Components of Pay to Retired Partners

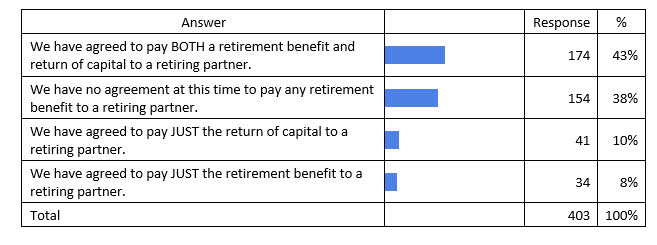

We asked multi-owner firms what describes their firms’ agreements to pay retired partners—whether the agreement included both a retirement benefit and a return of capital, one or the other, or neither. The following table summarizes the results, based on data from 403 firms:

Thirty-eight percent of the firms responding have no agreement at this time to pay any retirement benefit to a retiring partner. Once partners begin to retire, our experience has shown that many firms without an agreement in place prior to the retirements will be mired in unnecessary rounds of negotiations that often lead not only to some level of acrimony among the parties, but often lead to bad deals for the firm as well.

Thirty-eight percent of the firms responding have no agreement at this time to pay any retirement benefit to a retiring partner. Once partners begin to retire, our experience has shown that many firms without an agreement in place prior to the retirements will be mired in unnecessary rounds of negotiations that often lead not only to some level of acrimony among the parties, but often lead to bad deals for the firm as well.

When the 154 firms without an agreement to pay retirement benefits are removed from the foregoing statistics, we find that 70% (174 of the remaining 249) have agreed to pay both a retirement benefit and return of capital to retiring partners, with the other 30% nearly evenly split between those paying only one or the other.

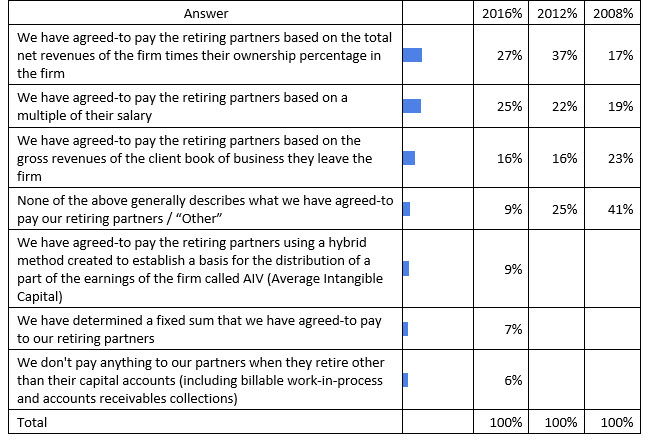

Which general methods has your firm agreed to use to determine the amount owed to retiring partners?

This year, 252 firms answered the survey question regarding methods used to determine the amount owed to retiring partners. The following table shows comparisons with the previous two surveys. Because of the additional answer options provided this year, based partly on “other” responses from past surveys and current practices in the profession, there is less comparability from survey to survey with respect to “other” and the newly listed, less common methods used. However, the three primary methods used over the last 12 years continue to dominate.

Consistent with prior years, the larger the firm, the more likely they use a multiple of salary (or sometimes translated into some kind of formula based on units, etc.) to determine the amount owed to retiring partners. The use of client book to determine value declines as the size of the firm grows. The use of ownership interest times net revenues grows as firms get larger and then drops as the firms start shifting to a multiple of salary approach. This usually occurs when ownership is sufficiently diffused and salary becomes a more meaningful indication of a partner’s value.

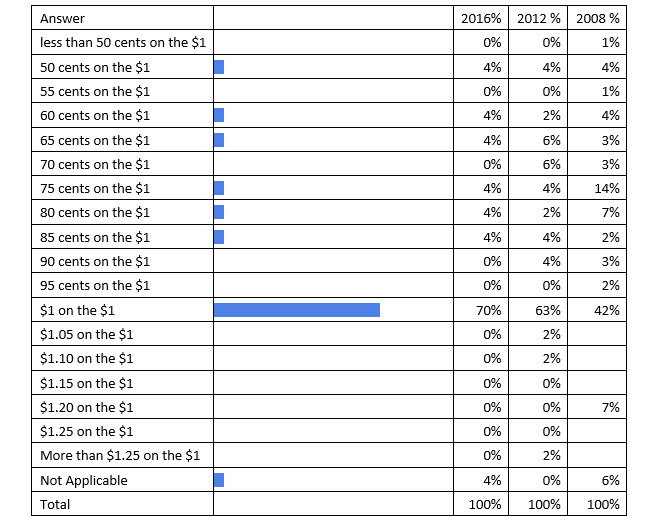

Which best approximates how you value the client book to calculate the retirement benefit?

For the 41 firms using client book (the revenues from the client book of business they leave the firm) to value a retiring partner’s benefit, the trend toward $1 of benefit value for one dollar of client revenue continues, as does the trend in decreasing use of values greater than $1 for $1 of revenue.

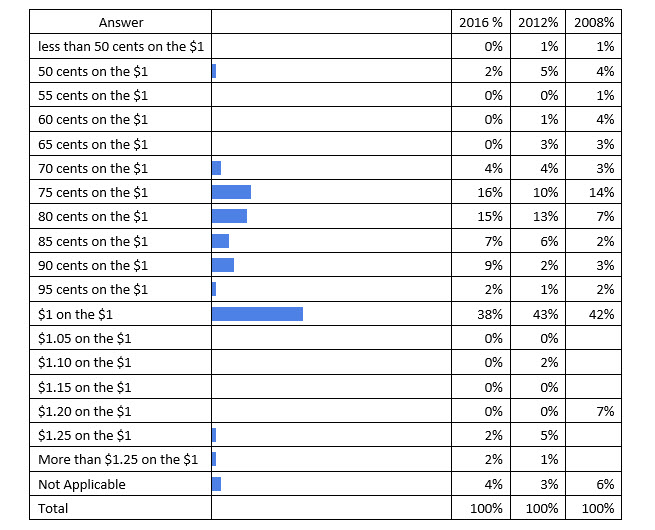

Which best approximates how you value the ownership interest in the firm to calculate the retirement benefit?

Of the 55 responses to this question, 38% of firms using the ownership interest approach for valuing a retirement benefit set the value at $1 for $1 of revenue. Fifty-one percent (4% + 16% + 15% + 7% + 9%) of the firms are valuing the retirement at between 70ȼ and 90ȼ per dollar of revenue. Within that broad range, 31% (16% + 15%) of the responding firms are using a value ranging between 75ȼ and 80ȼ on the dollar. Trends over the years show that firms are moving away from values outside of the 70ȼ to 90ȼ per dollar range.

Which best approximates the magnitude of the multiplier you use pertaining to average salary to calculate the retirement benefit?

The percentage of 63 firms using a multiplier from 2.0 to 3.0 times average salary has held somewhat steady over the last three surveys. The largest firms will skew more towards 2.5 times average salary, whereas the firms that ranged in this survey from 51 to less than 201 FTEs tended to lean toward 3 times average salary.

There has been a trend toward shifting from the upper end of this range (3.0 times) to 2.0 to 3.0 times average salary. We believe part of the reason for the trend toward lower multiples for larger firms is due to past, relatively high compensation of partners in past decade (although the economy was down in 2008, many firms did very well before and during the recession and that success has continued through today). Trends toward lower ranges of value in general, under any of the three most common methods of valuation, would make sense when considering the growing concern about potentially large financial burdens the firm will be taking on with upcoming partner retirements. Partner retirement and related succession management concerns, such as development of the next tier of leaders and ensuring a strong bench of staff at every level, coupled with any uncertainty about upcoming financial burdens, would tend to have a dampening effect on the magnitude of calculations used for retirement benefit.

We will pick up at this point in the survey the for our next column as the conversation moves to reviewing how firms might adjust the original valuation benefit based on actions or inactions of the retiring partner. As you will see as more of the survey results are shared, our profession will likely undergo an amazing amount of change during the next 5-7 years as baby boomers start to retire-in-force. And like all change, some doors will begin to close as other windows and doors will be opening unveiling new opportunities for looking for them and positioned well to seize them.

Download

| File |

|---|

| PCPS Succession Institute 2016 Succession Survey Results for Multi-Owner Firms-Part 3 |

We help organizations implement their unique strategies by:

• Working with them through the tough issues, and

• Customizing responses to address root causes, rather than merely treating symptoms.