PCPS Succession Institute 2016 Succession Survey Results for Multi-Owner Firms Part 2

This article summarizes selected results of the Private Companies Practice Session (PCPS) and Succession Institute (SI) 2016 Succession Planning Survey (the full survey results available through the PCPS Resource Center). This is the fourth such survey conducted since 2004. Part 1 of this column series covered the results for Solo Practitioners and Sole Proprietors. Part 2 starts with the 435 Multi-Owner firms responding and will take several columns for us to cover even the highlights of the survey. The following tables and commentary summarize the results and our conclusions, succession plans through sale or merger of their practices.

Survey Demographics

This year’s survey was launched April 28th and closed on May 17th, 2016. The survey was expected to take 25 to 50 minutes to complete, compared to our 2012 survey’s 10 to 20 minutes. Because of this additional time requirement, we expected far fewer completed responses, so we were very pleased with the final participation numbers. As the graphic below shows, we had 819 from US firms, which included 68 from US Solo Practitioners, 316 from US Sole Proprietors (read our last column on Solos and Soles for more details on these two groups) and 435 from US Multi-Owner firms. The US responses in this survey amounted to roughly 87% of the responses we achieved in 2012 (941 responses), roughly 172% of the responses for 2008 (476 responses) and 177% of the responses for 2004 (463 responses)

Of the 819 US responses, participant demographics ranged from:

• .5 to 973 Full Time Equivalents (FTEs)

• $25,000 in CPA firm net revenues to $160 million in CPA firm net revenues

• zero to $85 million in net revenues from other entities,

• $10,000 to $1,500,000 average owners’ compensation

• 1 to 100 equity owners

• zero to 75 non-equity owners

• zero to 650 accounting staff

• zero to 210 administrative and paraprofessional staff

Which of the following best describes your firm?

Who Responded to this Survey?

A total of 435 multi-owner firms responded to this survey. The following tables provide some additional information as to who responded to the survey. Anytime our surveys ask for specific dollar amounts, such as revenues, partner compensation, etc., as often happens, many survey participants do not complete these sections. The following two tables break down the number of responses by Net Annual Revenue and by Full Time Equivalents (FTEs).

This first table shows the number of respondents (371 total) sorted by each revenue category listed below.

This next table shows average Net Annual Revenues by FTE categories (362 responses).

Average annual owner compensation by firm size in FTEs for the most recent complete year were reported as follows.

Average annual owner compensation by firm size in FTEs for the most recent complete year were reported as follows.

Existence of Succession Plans

Over the years, the percentage of multi-owner firms that have a written, approved succession plan in place has increased gradually during three out of the last four surveys, from 25% in 2004, to 35% in 2008 and 46% in 2012, with a slight reduction in 2016 to 44%. Given the potential selection bias in the survey, the 2016 percentage can be considered essentially the same as 2012. While the trend has been positive, and it is clear that partners are delaying retirement by wanting to work longer, the fact that our surveys have never shown more firms with a succession plan than without one is of concern. However, while we don’t believe nearly enough firms have a written, approved succession plan in place, they are making positive strides in addressing succession issues as part of their firm management and infrastructure improvement processes. See the two tables below for the break down regarding succession plans both for 2016 as well as for the past 12 years, covered through four successive quadrennial surveys.

We currently have a written, approved succession plan in place:

The following table shows that the smaller the firm, the less likely they are to have a written and approved plan in place. Simply put, less than 50% of firms with less than 26 FTEs have succession plans in place, and 61% or higher of firms with 26 FTEs or more have succession plans in place, with firms above 101 FTEs at 76% and firms above 201 FTEs at 100%.

There can be a variety of reasons that smaller firms do not have a succession plan in place, not the least of which is that the smaller firms may be at a point in their life cycle where they are operating under more of a silo or “Eat What You Kill” business model. Under this type of model, each owner can decide when he/she is going to retire, and under what conditions/terms each will retire. They then can individually decide to sell off their own book of business to whomever they can at whatever price can be negotiated at that time (maybe these owners can sell their book of business or some portion of it to their existing partners, or maybe they will have to sell their clients to another firm entirely). No matter how you operate, however, we believe that every partner (even better if it is the whole firm), should be making arrangements now (ahead of time) to deal with succession, even if that plan only addresses a crisis situation. Logically, it is much more preferable that the plan also deal with planned departures and succession management as well as well as crises.

Progress Made with Succession Plans

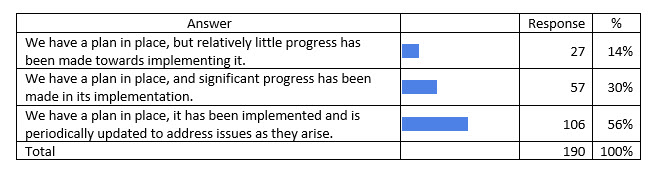

For those firms that do have a written succession plan in place, we asked for an indication of their current progress with respect to actual implementation of their succession plan. 56% of firms with succession plans indicated that they do have a plan in place and it is periodically updated to address issues as they arise. Another 30% have a plan in place and significant process has been made in its implementation. This total of 86% of firms (of the 44% that have plans in place) is a slight improvement over 2012. However, as you will see in the table by firm size, much more progress has been made in this area with larger firms.

The following best describes our progress with our current succession plan:

Here are the answers from 2016 compared with 2012 responses:

Here are the answers from 2016 compared with 2012 responses:

Firms with 101 or more employees are more likely to have plans in place that are either partially or fully implemented. None of that group said that “a plan is in place, but relatively little progress has been made towards implementing it.”

Firms with 101 or more employees are more likely to have plans in place that are either partially or fully implemented. None of that group said that “a plan is in place, but relatively little progress has been made towards implementing it.”

The smaller the firm in size, the more likely it is that the firm has a plan but relatively little progress has been made towards its implementation.

The smaller the firm in size, the more likely it is that the firm has a plan but relatively little progress has been made towards its implementation.

Status of Succession Planning

For firms that do not have a succession plan in place, the percentage of responses indicating no perceived need to have a plan has decreased over the past 12 years from 19% to 5% which is a great trend. 45% (34% + 11%) of the firms have started a plan or have one in draft form, ready for approval.

As to the status of our succession plan, we:

The problem is that four years ago, 42% (30% + 12%) of the respondents said that they had started their succession plan or the plan was in draft stage just prior to approval, and 8 years ago that number was 44% (35% + 9%). Based on the survey findings over the past decade, given these high percentages of firms in the final stages of pulling their succession plan together, the number of firms that have written approved succession plans in place should clearly be trending up instead of holding about the same. What this says to us is that there is a giant chasm between starting a succession plan or drafting one, and actually putting it in place.

The problem is that four years ago, 42% (30% + 12%) of the respondents said that they had started their succession plan or the plan was in draft stage just prior to approval, and 8 years ago that number was 44% (35% + 9%). Based on the survey findings over the past decade, given these high percentages of firms in the final stages of pulling their succession plan together, the number of firms that have written approved succession plans in place should clearly be trending up instead of holding about the same. What this says to us is that there is a giant chasm between starting a succession plan or drafting one, and actually putting it in place.

None of the responding firms with more than 16 FTEs (down from 50 FTEs in 2012) or above $3.5 million in revenue (down from $8 million in net annual revenues in 2012) answered that they do not feel the need to have a plan. This makes sense inasmuch as the larger the firm, the more critical it is to have plans, policies, agreements and other infrastructure in place to support the longevity and vitality of the firm over the long-term. But this is a great example of the fact that, while some of the statistics regarding succession in this survey by themselves are not showing significant positive movement, the awareness of the need for succession planning has moved downstream in firm size from $8 million and above to $3.5 million and above, and from 50 FTEs and above down to 16 FTEs and above.

Do you expect succession planning to be a significant issue for your firm in the next 10 years?

84% (14% + 34% + 18% + 8%) of the 434 multi-owner firms who responded to this question felt that succession planning will be a significant issue for the firm in the next 10 years. That number has grown by 5% since the 2012 survey. It is interesting to note that, although 84% of firms believe succession will be a big issue for them in the next decade, only 44% of the firms have a plan in place.

84% (14% + 34% + 18% + 8%) of the 434 multi-owner firms who responded to this question felt that succession planning will be a significant issue for the firm in the next 10 years. That number has grown by 5% since the 2012 survey. It is interesting to note that, although 84% of firms believe succession will be a big issue for them in the next decade, only 44% of the firms have a plan in place.

Timing of our succession planning challenges:

Right now, about a quarter of the firms that said they expect to have significant succession challenges said they are currently working through these issues. Only 14% are worried about the next 1 to 2 years, which is down significantly from the last two surveys. 34% expect succession challenges in the next 3 to 5 years, which is significantly up from any of the previous surveys. But when you look at this table, it seems to be a point-in-time reference as to the state of firms rather than indicating any consistent trends.

Right now, about a quarter of the firms that said they expect to have significant succession challenges said they are currently working through these issues. Only 14% are worried about the next 1 to 2 years, which is down significantly from the last two surveys. 34% expect succession challenges in the next 3 to 5 years, which is significantly up from any of the previous surveys. But when you look at this table, it seems to be a point-in-time reference as to the state of firms rather than indicating any consistent trends.

One of the potential answers as to why the horizon of 3 to 5 years is showing as the highest timeframe for potential succession challenges is that a great number of partners are unwilling to give a final indication as to when they plan on retiring. And even more so, as to whether they plan to partially retire or fully retire. So, as in the past, we find the 3 to 5-year window to be that perfect time to quote due to its total lack of accountability. A partner can inform the firm that he/she is leaving near-term, but the timeframe is far enough away that neither the partner nor the firm feels like there is a need for current, specific action to address this change.

Equity Ownership Soon to Retire

Next, participants were asked how many owners were planning to retire in the next five years, and what the approximate equity ownership percentage of those retiring in this five-year period is, starting with 2016 retirements.

Out of 363 respondents, here is how “the number of partners” leaving broke down.

How many equity partners/owners are planning to retire in the next five years?

74% (37% + 29% + 3% + 3% + 1% + 1%) of the firms responding to this question will have one or more partners retiring in the next 5 years, with 37% (29% + 3% + 3% + 1% + 1%) having two or more retiring in that same timeframe.

Drilling down further, we asked what ownership percentage was likely to be transferred during the period. Just taking a broad view, our series of questions on this topic first provided an average amount of ownership expected to be transferred over the next five-years. In each of the following years, of the firms surveyed, these percentages of equity ownership on average are expected to retire and will need to be transitioned to other owners:

- In 2016, an average of 5% of the ownership is expected to transfer

- In 2017, an average of 5% of the ownership is expected to transfer

- In 2018, an average of 7% of the ownership is expected to transfer

- In 2019, an average of 6% of the ownership is expected to transfer

- In 2020, an average of 12% of the ownership is expected to transfer

This totals 35%, which means that the voting in firms can significantly change as new partners are added to leadership or existing partners obtain greater voting rights. Either way, 35% can be a game changer by the fact that this block of ownership can now veto almost any action presented in any super-majority vote. But remember, this is an average. So, out of the 363 firms that filled out this part of the survey, most in any given year would have no partners leaving (so zero percent ownership would be transitioning for them), and then some will have partners leaving with small amounts of ownership and a few leaving with a large amount of ownership creating a low overall average. So we dug deeper into the data to come up with this additional insight:

- In 2016, 8.6% of the respondents said 25% or more of the ownership of their firm would be retiring, and 4% would have 50% or more of the ownership retiring

- In 2017, 8.8% of the respondents said 25% or more of the ownership of their firm would be retiring, and 3.6% would have 50% or more of the ownership retiring

- In 2018, 11.6% of the respondents said 25% or more of the ownership of their firm would be retiring, and 5% would have 50% or more of the ownership retiring

- In 2019, 9.3% of the respondents said 25% or more of the ownership of their firm would be retiring, and 4.3% would have 50% or more of the ownership retiring

- In 2020, 19.2% of the respondents said 25% or more of the ownership of their firm would be retiring, and 10.9% would have 50% or more of the ownership retiring

This creates a far more urgent picture regarding the succession landscape for our profession. If you total up the next 5 years, this data shows that 57.5% (8.6% + 8.8% +11.6% + 9.3% + 19.2%) of the firms said they would have 25% or more of their ownership in transition and 27.8% (4% + 3.6% + 5% + 4.3% + 10.9%) will have 50% or more of their ownership in transition. In other words, a quarter of all multi-owner firms will have a controlling interest in the firm changing hands during this time period. This means that firms need to get their act together regarding the next generation of leadership or merger mania will be the only option left. It is hard enough for firms to withstand a 25% change in ownership without some serious changes, updates and formality developed throughout the firm’s infrastructure, and especially in critical areas such as governance, accountability and compensation. For any of those firms with minimal to partial succession plans in place, a formidable situation will evolve creating a questionable likelihood of the new internal leadership being able to successfully take over, be able to sustain the firm’s profitability and unity, and be in a position to pay off the large retirement benefits accompanying large ownership blocks of retiring owners.

Ownership Positions and Expected Changes

This next section takes a quick look at what positions firms have created as a market-facing (in other words, all of these positions would be perceived by the clients of the firm to be partners of the firm) partner-equivalent position to augment their leadership ranks. Additionally, we wanted to get a perspective as to whether firms believe that they have the right number of partners, are over-partnered or under-partnered.

Besides equity partners, which leadership positions does your firm recognize as a partner equivalent?

This was a “select all that apply” question, which 186 people responded to. Of those firms, over 50% of them have added the position of non-equity partner to their leadership group, 35% have added income partners, 21% principals, and 14% directors. Usually a non-equity partner, income partner or principal would not own equity in the firm, except perhaps some minimal amount required under state statute. But in our experience, which was not a question asked in this survey, there are a number of firms where the title of principal, and more often the title of director do not differentiate as to whether the partner owns equity or not.

This was a “select all that apply” question, which 186 people responded to. Of those firms, over 50% of them have added the position of non-equity partner to their leadership group, 35% have added income partners, 21% principals, and 14% directors. Usually a non-equity partner, income partner or principal would not own equity in the firm, except perhaps some minimal amount required under state statute. But in our experience, which was not a question asked in this survey, there are a number of firms where the title of principal, and more often the title of director do not differentiate as to whether the partner owns equity or not.

Which best describes your firm's status with respect to your total number of partners?

The above table and the next one provide a great deal of insight. 68% of the respondents say they have the right number of partners, 19% say they have too many partners, and 13% say they have too few partners.

The above table and the next one provide a great deal of insight. 68% of the respondents say they have the right number of partners, 19% say they have too many partners, and 13% say they have too few partners.

Now, given the data above that 74% of these firms with have at least one partner retiring, and 37% will have two or more partners retiring, that 44% of the firms have succession plans in place, and 54% of firms have created non-equity partner positions (with others creating additional partner equivalent, non-equity positions), we would have expected to see a higher percentage of firms that said they are over-partnered at this time. The good news is that firms can have the right number of partners now, but be focusing on increasing capacity, delegation and leverage within the firm, and they will be in a great position to retire partners, not have to add any new ones, and still have the right number of partners. So, not being over-partnered at this point is not a problem if the firm is well underway toward fixing some basic capacity problems now. Unfortunately, the firm initiative to create capacity and push work down usually takes 3 to 5 years to implement, so it is not something you can put in place the last minute before a partner retires.

Based on your projected growth over the next five years, which best describes your firm's status with respect to your total number of partners?

Now take a look at the above table. We asked firms about their growth expectations over the next five years. Given their expected growth, we asked about expectations regarding the size of their partner group 51% of the firms expect to add new partners by the end of five years. Obviously, the larger their expected growth, the more that adding partners is an expected response. But if the growth expected is fairly conservative, then this is not always the answer we would suggest to our firms. We are proposing that our clients increase staffing, build greater competencies at every level in the firm, push work down wherever possible, train-train-train, and shift smaller clients down to managers to manage. This is because the most profitable focus of firms is to increase the size of books partners and managers can manage, thereby requiring fewer partners to sustain a growing firm. This leveraged approach allows partners to retire while making it easier for the remaining partners to pay them off and actually allows the remaining partners to make more money than the departing partners did. But it requires a firm to grow their average books managed per partner from wherever they are now to double that over the next five years. This approach not only makes succession easier (because we are not scrambling to find partner replacements), but the profitability far more robust.

This is why we see the 35% response rate from the firms that don’t expect to add partners while growing as being so positive. As well, it is why we see as positive the expectation that 14% of the firms expect to see a decrease in partners. For the 19% that feel they have too many partners now in the first question regarding number of partners, it makes sense that 14% in the second question expect to see the size of their partner group decrease. Our concern is that some of the 51% that plan to add partners are doing so under the old-school and less profitable idea of replacing a retiring partner with a new partner rather than revamping the capacity and workload of the existing partners.

As many of you know from reading our books and listening to us (Dom and Bill) speak, what we find in the marketplace is that most partners, based on the level of work they are doing every day -- at least partially, and some nearly completely -- simply fill the role of manager. Therefore, if that is occurring, then most managers in those situations would be expected to fill the role of supervisor, and this working below your level trickles down throughout every level in the firm. By getting partners to only focus on partner-level work and delegate all of their current manager level work down to managers, and enforcing the proper alignment of work with everyone in the firm, most firms actually end up being over-partnered. But unfortunately, they are so short-staffed that this is not possible without changing the culture of the firm and the accountability of everyone for these new expectations.

Firm Infrastructure – Policies and Procedures

Because having the appropriate infrastructure (policies, procedures and agreements, for example) in place is necessary for the successful continuation of a firm, the survey asked participants what sort of formal agreements and policies they currently have in place.

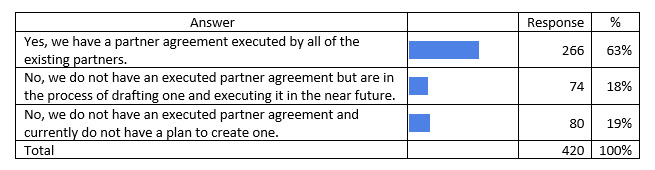

Do you have a partner agreement executed by all of the existing partners which include common policies like agreed upon retirement benefits, partner admission terms, partner termination, etc.?

To no surprise, the smaller the firm, the less likely they will have a partner agreement in place (37% at less than 8 FTEs, as compared to 100% at more than 100 FTEs). And although the smaller the firm, the more informal the operations tend to be, it is critical that they institute more formality by way of agreements, policies and procedures to allow the firm to grow and prosper while avoiding misunderstandings which can lead to unnecessary conflict, often very damaging conflict, about such issues in the future.

Which standard operating policies/procedures has your firm formally developed and documented with powers, roles, responsibilities, and limitations?

This was a “select all that apply” question, which has 397 respondents answering it. The surprising result from this question was that there was no improvement, and as a matter of fact, based on 2012 data, many of the answers are in a decline (many issues were being addressed more frequently then than now).

This list of issues is what we believe should be addressed, at a minimum, in partner agreements and formal policies and procedures. The fact that the highest response was 63% among all of these issues is our biggest concern. Just to highlight a few issues, it seems that responses to all of these policies should be at the 90% level or higher (instead of where they fell in the survey results):

- In the event of death, agreed upon value of ownership and benefits required to buy out a partner and pay his or her estate (63%)

- Partner roles and responsibilities (51%)

- Agreed upon terms, conditions, benefits and damages for partners leaving the firm who take clients or employees (44%)

- Requirements for termination of a partner (41%)

- Vesting schedule and terms (age and years of service) needed to qualify a partner selling his or her ownership interest to earn retirement benefits (34%)

- Retired partner roles and responsibilities (13%)

We would expect to see positive responses of at least 50% or more for even the more operationally standard, mundane policies such as the two examples below:

- Expense management policy and oversight (29%)

- Nepotism policy (14%)

Our conclusion is that not only do far too many firms NOT have partner agreements (18% + 19% = 37%), but of those that do (63%), the agreements are not addressing many of the critical issues that commonly cause problems in successful CPA firms.

We will pick up at this point in the survey the for our next column as the conversation moves to Mandatory Retirement, Vesting, Valuation and so much more. As you will see as more of the survey results are revealed, reviewing highlights of the survey results regarding multi-owner firms, just as it did for Solo Practitioners and Sole Proprietors, will reflect the state of our profession regarding succession and why you can expect dramatic changes over the next 5 years.

Download

| File |

|---|

| PCPS Succession Institute 2016 Succession Survey Results for Multi-Owner Firms Part 2 |

We help organizations implement their unique strategies by:

• Working with them through the tough issues, and

• Customizing responses to address root causes, rather than merely treating symptoms.